What Is a Non-QM Loan? Types, Requirements & Who Qualifies

Every year, qualified borrowers get turned away by traditional lenders, not because they can't afford a home, but because their income looks unusual on paper. For borrowers like a freelancer earning $200,000 a year or a landlord whose rental portfolio generates strong cash flow, the requirements of a conventional or government-backed mortgage create a barrier unrelated to their actual ability to repay a loan. That's the problem non-QM loans were built to solve.

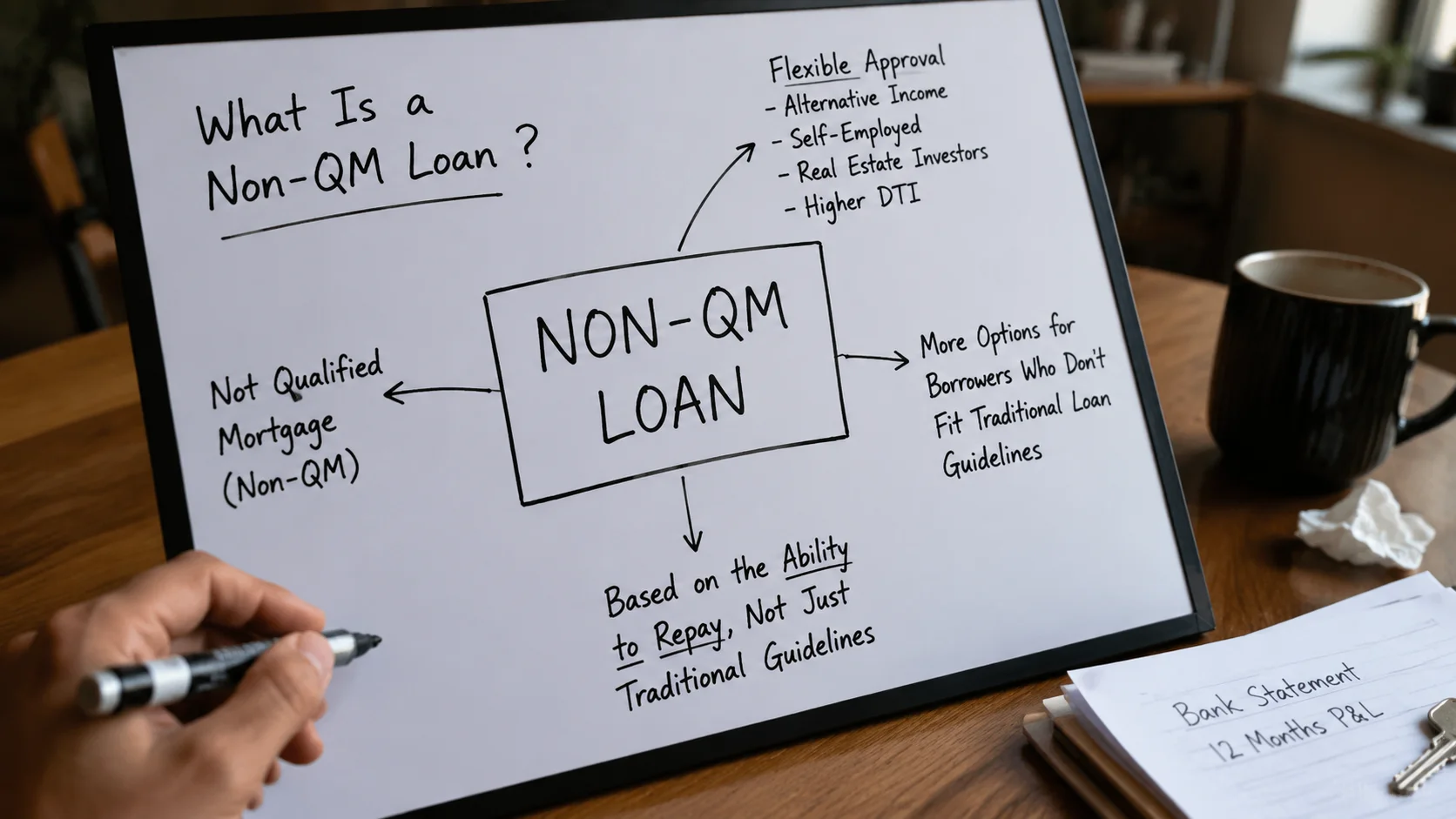

What Is a Non-QM Loan?

A non-QM loan (non-qualified mortgage) is a home financing product designed for borrowers who may not qualify for a traditional home loan due to their income, credit history, or documentation. It uses alternative underwriting criteria to assess your true ability to repay the loan, rather than forcing your financial life into a government-mandated checklist.

Non-QM doesn't mean no documentation or subprime. These loans require real evidence of repayment ability. Lenders can use bank statements, asset depletion, rental income, or other alternative income documentation instead of only W-2s and tax returns.

Qualified Mortgage vs. Non-Qualified Mortgage

After the 2008 financial crisis, the Consumer Financial Protection Bureau (CFPB) established the Qualified Mortgage (QM) rule under the Dodd-Frank Act. The rule gave lenders legal protection from ability-to-repay lawsuits, provided their loans met specific criteria. A QM loan is a loan that the lender verified the borrower can genuinely repay.

Qualified Mortgage Requirements

- Debt-to-income ratio (DTI) no higher than 43% (some GSE loans use a flexible cap via automated underwriting)

- Full income documentation, typically W-2s and two years of federal tax returns

- No excessive upfront points and fees (capped at 3% of the loan amount)

- No balloon payments, negative amortization, or interest-only payments in most cases

- Loan term of 30 years or less

How Non-QM Loan Works

A non-QM mortgage steps outside the QM rule's boundaries. It uses alternative mortgage underwriting methods, different income documentation, flexible DTI analysis, or property-income-based qualification, to confirm if the borrower can repay the loan.

Who Can Benefit from a Non-Qualified Mortgage?

Non-QM loans are not for borrowers who can't afford a home, they're for borrowers whose financial picture doesn't translate into standard documentation.

1. Self-Employed Borrowers and Business Owners

Small business owners, freelancers, and contractors write off significant expenses against their income. The problem is that those deductions reduce taxable income on the tax returns that a conventional lender reads. A borrower whose business grosses $300,000 annually may show $90,000 in net income after deductions, triggering a denial on home affordability grounds even though their cash flow tells a completely different story.

2. Real Estate Investors

Investors with multiple rental properties often carry a high overall debt-to-income ratio (DTI) on paper, even when each property generates positive cash flow. A DSCR Loan (Debt Service Coverage Ratio) qualifies the loan based on the subject property's rental income relative to its monthly mortgage payment, not the borrower's personal income.

3. Asset-Rich Borrowers with Limited Income

Some borrowers hold substantial assets, like brokerage accounts, retirement portfolios, and real estate equity, but draw limited earned income. Asset depletion loans convert liquid assets into a qualifying monthly income figure. For example, $1.2 million in liquid assets divided over 360 months (30 years) equals $3,333/month in qualifying income.

4. Borrowers with Recent Credit Events

A bankruptcy, foreclosure, or short sale doesn't necessarily mean years of waiting. Some non-QM programs allow a home purchase loan as soon as one day after a bankruptcy discharge or foreclosure at a higher interest rate, but with a viable path back into homeownership. The rate premium decreases as time and credit recovery put more distance between the borrower and the event.

5. Foreign Nationals

Non-U.S. residents without a Social Security number or established U.S. credit history can often qualify for non-QM financing using foreign credit reports, ITIN numbers, international bank statements, or verified offshore assets. Loan-to-value ratios are typically more conservative (60–70% LTV), and documentation requirements are adapted to the borrower's country of origin.

6. Jumbo Borrowers with Complex or Mixed Income

High-value purchases that exceed conforming loan limits present a challenge when the borrower's income is a blend of salary, business distributions, rental income, capital gains, and bonuses. Non-QM jumbo programs accommodate this complexity without the rigid documentation hierarchy of a conforming jumbo loan.

Non-QM Loan Requirements

While non-QM loan requirements vary by lender and loan type, most programs evaluate borrower eligibility across several key dimensions. Understanding these upfront puts you in a much stronger position during the mortgage application process.

Income Documentation

- Bank statement programs: 12 or 24 months of deposits, personal or business account

- DSCR programs: Property rent roll or market rent analysis; no personal income docs required

- Asset depletion: Verified liquid asset statements (investment accounts, savings, retirement)

- 1099 programs: 1099s averaged over 12–24 months; some lenders accept 12 months only

- P&L only: CPA-prepared profit & loss, typically covering the most recent 12 months

Credit Score

Most non-qualified mortgage programs require a minimum of 620–680 credit score, though some DSCR programs work with 580+ when the DSCR ratio is strong, and the LTV is conservative. Unlike conventional loans, credit score is one factor in a broader risk picture.

Start your mortgage journey with clear guidance and real numbers. See what you qualify for today.

Down Payment and Loan-to-Value Ratio (LTV)

The loan-to-value ratio (LTV) is a critical variable. Non-QM programs typically require 10–30% down, depending on loan type and risk profile. A lower LTV reduces lender risk and unlocks better rates. Borrowers with recent credit events or lower credit scores are generally required to bring more equity.

Debt-to-Income Ratio (DTI) and Housing Expense Ratio

Non-QM programs often allow a debt-to-income ratio (DTI) above the conventional 43% threshold. Lenders also evaluate the housing expense ratio (monthly housing costs as a percentage of gross income) separately. For most programs, keeping the housing expense ratio below 40–43% is a good target even when the overall DTI is higher.

Cash Reserves

Cash reserves are heavily weighted in non-QM underwriting. Most programs require 6–24 months of principal, interest, taxes, and insurance (PITI) in liquid reserves after closing. For DSCR programs, some lenders require 3–6 months per financed property in the portfolio.

Property Type

Non-QM loans apply across owner-occupied property (primary residence), second homes, and investment properties. For a primary residence, the lender evaluates personal income and the housing expense ratio. For investment properties, the analysis shifts to the property's income performance.

Non-QM Loan Rates

Non-QM rates run higher than conventional or FHA rates. The premium exists because non-QM lenders step outside the QM safe harbor, and because these loans are held in portfolio or sold to private investors rather than sold to Fannie Mae or Freddie Mac.

As a general benchmark, expect non-QM rates to run approximately 0.5% to 2.0% above comparable conventional rates. The exact rates depend on:

- Loan type: DSCR and bank statement loans typically carry a smaller premium than post-credit-event programs

- LTV: A lower loan-to-value ratio (LTV) directly reduces your rate

- Credit score: Every 20–40 point improvement in your credit score can reduce your rate by 0.125–0.25%

- Cash reserves: Demonstrating 12+ months of reserves often improves pricing at the underwriting level

- Right Mortgage Lender: Non-QM pricing varies more widely across lenders than conventional pricing

What Are the Drawbacks of a Non-QM Loan?

Higher Interest Rates

The 0.5–2.0% rate premium is real and compounds over a 30-year loan. On a $500,000 loan, a 1.5% rate difference equals roughly $450/month more in payment and over $160,000 in additional interest over the full loan term.

Larger Down Payment Required

Most non-QM programs require 10–30% down, compared to 3–5% for FHA or conventional conforming loans. This can be a significant barrier for borrowers who don't have substantial liquid assets beyond their income.

Prepayment Penalties

Some non-QM loan products include prepayment penalties. If you plan to sell or refinance within 1–3 years, these penalties can ruin the financial benefit significantly.

Fewer Lenders and Less Price Transparency

Non-QM lending is not offered by every bank or credit union. The smaller pool of lenders means less competitive pressure on pricing and less borrower familiarity with the terms.

Loan Servicing Changes

Non-QM loans are often sold in the secondary market to institutional investors. Servicing can transfer to a new servicer after closing. This doesn't change your loan terms, but it's worth being aware that the company you make payments to may not be the company that originated your loan.

No Government Backing

Because these loans fall outside GSE and FHA/VA programs, they don't carry government backing. For borrowers who later want to apply for assumption-eligible or government-backed refinancing, there's an additional step back into QM territory.

How to Get a Non-QM Loan

Step 1: Identify Your Borrower Profile and Matching Loan Type

Start with your profile, then identify the program. Applying for the wrong product wastes time and creates an unnecessary inquiry on your credit report.

Step 2: Organize Alternative Documentation

Pull together the documents specific to your program: 12–24 months of bank statements, 1099s, a CPA-prepared P&L, or a property rent roll.

Step 3: Run Your Own Numbers First

Calculate your debt-to-income ratio (DTI), estimate your housing expense ratio, and map your available down payment against target LTVs.

Step 4: Work with a Non-QM Specialist Lender

Non-QM loan programs require lenders who underwrite these products daily, not retail banks that treat non-QM as an occasional exception.

Step 5: Proceed Through the Mortgage Application Process

The formal mortgage application process for non-QM follows the same core stages as any mortgage: application, pre-approval, rate lock, appraisal, full underwriting, and closing.

Step 6: Plan Your Exit Strategy

If your non-QM rate is higher than you'd like long-term, build a timeline: when will your income documentation stabilize? When will your LTV improve through appreciation or paydown?

Where Can You Get a Non-QM Loan?

Non-QM Specialist Lenders

These lenders have dedicated non-QM programs with in-house underwriting expertise. They move faster, offer broader product variety, and understand the nuances of alternative income documentation. Rize Mortgage falls into this category, with specific programs for DSCR investors, self-employed borrowers, and non-traditional earners.

Mortgage Brokers with Non-QM Access

Independent mortgage brokers may have access to multiple non-QM wholesale lenders, giving you a rate comparison across programs. The quality of service depends heavily on the broker's familiarity with non-QM underwriting requirements.

Banks and Credit Unions (Limited)

Some larger regional banks hold non-QM portfolio loans in-house, primarily jumbo programs for high-net-worth clients. Most retail banks and credit unions don't actively participate in non-QM lending.

Conclusion

A non-QM loan is not a fallback for unqualified borrowers. It's the correct tool for creditworthy borrowers whose financial reality doesn't fit inside a W-2 and two years of tax returns. Self-employed business owners, active real estate investors, high-net-worth individuals, foreign nationals, and borrowers rebuilding from a credit event all have a genuine case for non-qualified mortgage financing.

FAQs

1. What credit score do I need for a non-QM loan?

Most non-QM programs require a minimum of a 620–680 credit score. Some DSCR programs work with scores as low as 580 when the DSCR ratio is healthy (1.2+), and LTV is conservative (65–70%). Unlike conventional loans, credit score is one factor among several.

2. Are non-QM loans the same as subprime loans?

No. The 2008 crisis was driven by stated-income no-doc loans with no real verification, reckless LTVs, and borrowers who genuinely could not repay. Non-QM loans require real income verification, just through alternative documentation methods. All non-QM lenders are bound by the CFPB's Ability-to-Repay rule. They are a flexible product, not an unverified one.

3. Can I use a non-QM loan for an investment property?

Yes, it's one of the most common non-QM use cases. DSCR loans in particular are designed for investment properties. Qualification is based on the property's rental income relative to its debt payment, not your personal DTI.

4. How much do you need to put down on a non-QM loan?

Down payment requirements for non-QM loans are generally higher than those for conventional loans. For a primary residence, most programs require 10–20%. For investment properties, expect 20–30% down. The exact requirement depends on your credit score, the loan type, and which non-QM program your lender is using.

5. Can I refinance out of a non-QM loan later?

Yes, and this is a common, deliberate strategy. Many borrowers use a non-QM loan as a bridge: buy now, then refinance into a conventional QM product within 12–36 months once income documentation is cleaner, the LTV improves, or a credit event ages off. Check prepayment penalty windows before signing; a 3-year step-down penalty can affect the refinance math.

Start your mortgage journey with clear guidance and real numbers. See what you qualify for today.